A conversation more about balance, not bets.

“Shyam, Is My Portfolio Really Complete?”

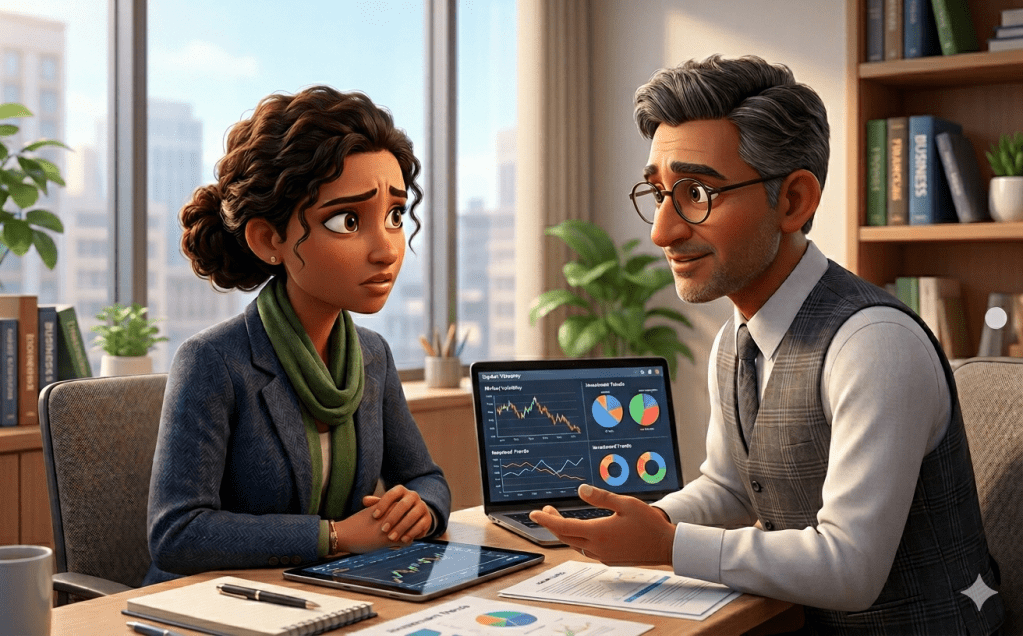

Diya had been investing for nearly eight years. Disciplined SIPs, a solid mix of large cap and flexi cap funds, some gold on the side. Every month, without fail, the money went in. She was proud of that.

But sitting across from her financial planner Shyam one evening, she couldn’t shake a quiet unease.

“Everything looks fine on paper,” she said, scrolling through her portfolio. “But somehow it doesn’t feel complete.”

Shyam nodded. He knew exactly what she meant.

“Diya, can I ask you something first?”

“Sure.”

“How many years have you been investing?”

“Eight years. Almost nine.”

“And in those eight years, have you ever had a year where you felt your portfolio was working really hard — and another year where it just felt stuck?”

She laughed. “Last year was great. This year…” she trailed off.

“This year Nifty is down. And that’s perfectly okay — that’s how markets work. India’s growth story is absolutely intact. The demographics, the infrastructure push, the consumption boom — none of that has changed. Your core Indian portfolio is doing exactly what it should be doing over the long term.”

Diya looked slightly relieved.

“But here’s my question,” Shyam continued. “While your portfolio was stuck this year — do you know what was happening outside India?”

She shook her head.

Shyam turned his laptop around. A simple heat map. Country by country, year by year, showing which market led and which lagged over twenty-one years.

“Look at this. No single country has stayed on top for more than a few years at a stretch. America dominated one window. China exploded and then crashed. Japan surprised everyone. Taiwan came out of nowhere recently. India had its own brilliant phases.”

“So they all take turns,” Diya said.

“Exactly. And here’s the one number I want you to remember — over the last twenty-one years, the US S&P 500 has delivered roughly thirteen and a half percent annually when measured in Indian rupees.

Nifty 50 delivered around 12% over the same period. Almost identical returns. But one was happening entirely outside India, in different companies, different sectors, a completely different economic cycle.”

Diya leaned forward.

“So the returns are similar, but they don’t move together.”

“Now you’ve got it.”

“So what are you suggesting?” she asked. “That I move out of India?”

“Absolutely not,” Shyam said firmly. “Your India story is your foundation. Don’t touch it. 80 to 85% of your portfolio should stay exactly where it is — in the funds you trust, the SIPs you’ve built, the India growth story you’ve been backing for 8 years.”

“Then what are we talking about?”

“The remaining ten to twenty percent. That’s the conversation.”

He leaned back.

“Think of your portfolio like a house. Right now it’s beautifully built — solid walls, great structure, everything you need. But it has only one window. And that window faces India. What I’m suggesting is that you open one more window. Not to leave the house. Just to let in more light.”

Diya smiled at the analogy. “Okay. So what’s outside that window?”

“Companies and themes that simply don’t exist at scale on Indian exchanges. The technology that powers every smartphone on the planet. The chips that run artificial intelligence. The software platforms that a billion people use every single day. These are businesses growing at a pace that is genuinely hard to find anywhere else right now.”

“And Indian investors can access all of this?”

“Completely. Through simple mutual fund routes — no foreign accounts, no complexity. Your money goes in as rupees, it works internationally, and it comes back as rupees. Same SIP process you already know.”

“What does this actually do for my portfolio?” Diya asked.

Shyam picked up a pen.

“Three things. First, it smooths your journey. When Indian markets are going through a tough phase — like right now — that ten to twenty percent is potentially working hard elsewhere, cushioning the overall impact.”

“Like a shock absorber.”

“Exactly. Second, there’s a natural currency benefit. The rupee has historically weakened gradually against the dollar over time. So your international returns get a quiet boost just from that movement — without you doing anything.”

“And third?”

“You get exposure to the next big wave before it fully arrives in India. AI, semiconductors, global healthcare innovation — India will eventually benefit from all of these, but the companies building the core infrastructure are mostly listed abroad. Owning a small piece of that story early is just smart investing.”

Diya was quiet for a moment, looking at her phone screen — her portfolio, eight years of careful decisions staring back at her.

“I’ve spent so much energy choosing between large cap and mid cap, between growth and value, between fund A and fund B — all within India. I never once thought about whether I needed to step outside at all.”

“Most investors don’t,” Shyam said gently. “And honestly, the fact that you’ve stayed disciplined and kept investing through every market cycle — that’s the hardest part. You’ve already done the difficult work.”

“This is just the next chapter,” Diya said quietly.

“Exactly that. You’re not changing your story. You’re just making it a little bigger.”

She put her phone down and looked at him.

“10 to 20% Outside India. As a shield, not a shift.”

“That’s all it is,” Shyam said. “You keep everything you’ve built. You just add one layer of balance that works when your core portfolio needs a breather.”

Diya nodded slowly, the unease from earlier finally lifting.

“Why did nobody tell me this eight years ago?”

Shyam smiled.

“Better late than never. The good news is — you have decades of compounding still ahead of you. And now your portfolio is ready for all of them.”

This is a fictional conversation created for illustrative purposes and does not constitute investment advice. Please consult a SEBI registered financial advisor before making any investment decisions.

Disclaimer : For informational purposes only. This is not investment advice. Mutual fund investments are subject to market risks. Please consult your registered financial advisor before making investment decisions. Read all scheme related documents carefully before investing.